| |

|

|

|

|

The

Asian Face of the Global Recession |

| |

| Feb

10th 2009, C.P. Chandrasekhar and Jayati Ghosh |

|

Delegates

to the World Economic Forum at Davos this year came

despondent and left in despair. Both the discussions

and the new evidence released at and during the Forum

indicated that the global crisis was not just bad,

but worse than originally anticipated. One damaging

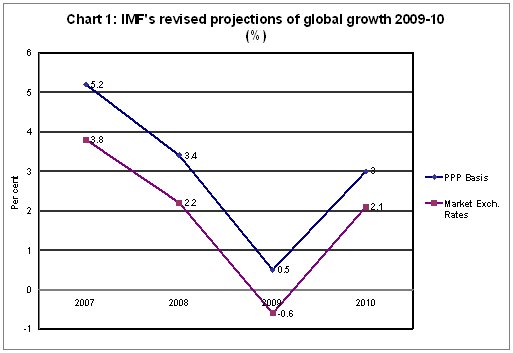

projection came from the IMF in its January 2009 Update

to the World Economic Outlook, which declared: ''Global

growth in 2009 is expected to fall to half percent

when measured in terms of purchasing power parity

and to turn negative when measured in terms of market

exchange rates. This represents a downward revision

of about 1¾ percentage point from the November

2008 WEO Update.'' (Chart 1)

Chart

1 >> Click

to Enlarge

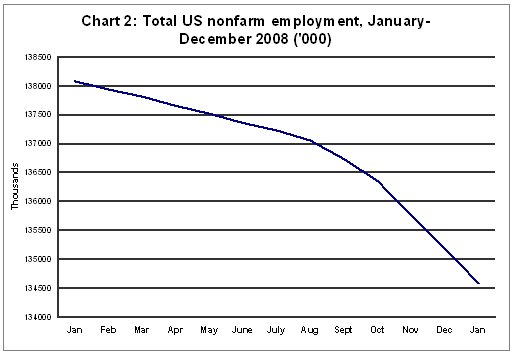

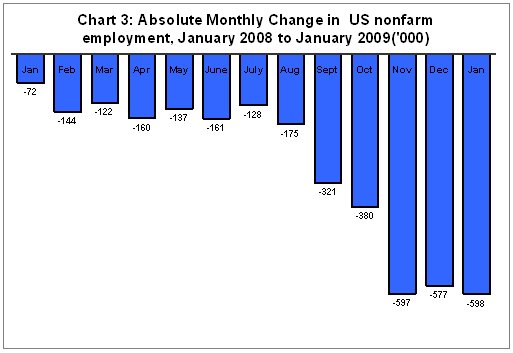

Moreover, data released in recent months by the US

Bureau of Labour Statistics points to a sharp fall

in non-farm employment in the US in recent months

(Chart 2). The monthly decline in nonfarm payroll

employment touched 598,000 in January when the unemployment

rate rose from 7.2 to 7.6 percent. Nonfarm employment

has declined by 3.6 million since the start of the

recession in December 2007, and about a half of this

decline occurred in the past 3 months (Chart 3). The

impact this would have on demand would only aggravate

the recession.

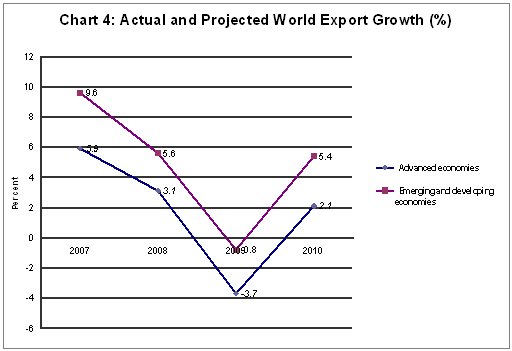

Finally, there is evidence that the global recession

led by contraction in the US is transmitting itself

through global trade. Export growth from the advanced

economies is projected to fall from a positive 5.9

per cent in 2007 and 3.1 per cent in 2008 to a negative

3.7 per cent in 2009. But this trend is not restricted

to the developed countries. The relevant figures for

the emerging and developing economies are 9.6 per

cent, 5.6 per cent and -0.8 per cent. (Chart 4). It

is small recompense that growth is projected to rebound

sharply in 2010. Such projections are suspect, since

the IMF has made it a habit of putting out optimistic

projections and then revising them downwards.

Chart

2 >> Click

to Enlarge

In fact, fear of a long recession stems not just from

the distressing developed country figures. It is also

triggered by evidence that the recessionary trend

is affecting Asia as well. Developing economies in

Asia, which as a group grew at 10.6 per cent and 7.8

per cent in 2007 and 2008, are now expected to grow

at just 5.5 per cent or 1.6 percentage points lower

than projected as recently as November last year.

Japan was already contracting by 0.3 per cent in 2008,

and is projected to see that figure falling to -2.6

per cent in 2009. But the three growth engines in

Asia, the ASEAN-5, China and India also now seem to

be badly affected by the crisis. The ASEAN-5 economies,

which grew at 6.3 and 5.4 per cent in 2007 and 2008,

are now projected to grow at 2.7 per cent in 2009

(down 1.5 percentage points from the November 2008

estimates). The corresponding figures for China are

13.0, 9.0 and 6.7 per cent (1.8 percentage points)

and for India are 9.3, 7.3 and 5.1 per cent (1.2 percentage

points). Moreover, the IMF has predicted a damaging

immediate future for South Korea, with its economy

projected to contract by 4 per cent this year.

Estimates from national sources and elsewhere are

less pessimistic than the IMF, but there is consensus

that outside the US it is Asia where the recession

is biting most. This is reflected in available estimates

on rising employment. According to official Chinese

figures, more than 20 million rural migrant workers

have lost their jobs and returned to their homes as

a result of the global economic crisis. According

to these estimates, by January 25, 15.3 per cent of

China's 130 million migrant workers had lost their

jobs and left coastal manufacturing centres to return

home. And the aggregate figure of migrant job loss

does not include those who stayed back in cities in

search of new jobs.

India too has made a feeble effort at estimating the

impact of the downturn on employment. An official

survey by the Labour Bureau focuses on 8 sectors (Mining,

Textile & Textile Garments, Metals & Metal

Products, Automobile, Gems & Jewellery, Construction,

Transport and the IT/BPO industry) to arrive at an

estimate of job loss as a result of the economic slowdown

in the country. In these sectors it sampled units

employing 10 or more workers to make its estimates.

Chart

3 >> Click

to Enlarge

The survey covered 2581 out of the sampled 3000 units

of which 1168 were from the Textile & Textile

Garments industry, followed by 752 in Metals &

Metal Products, 242 in IT/BPO, 132 in Automobiles,

104 in Gems & Jewellery, 103 in Transportation,

19 in Mining, and 61 in Construction. Based on this

limited sample, the total estimated employment in

all the sectors covered by the survey went down from

16.2 million during September 2008 to 15.7 million

during December 2008, implying a job loss of about

half a million (Table 1). The actual decline in employment

if coverage and method were better is likely to be

much higher.

However, the survey does suggest that employment fell

in every month during this period. After September,

2008 employment in all industries declined at an average

rate of 1.01 per cent per month. A comparison of employment

in export and non-export units indicates that employment

declined at an average monthly rate of 1.13 per cent

in the case of the former, as opposed to 0.81 per

cent in the latter (Table 2), pointing to the direct

role of the global slowdown.

Table

1: Trends in Average Employment, India (million) |

Period

|

Average

Employment |

%age

change |

September,08

|

16.2 |

|

|

October,08

|

16

|

-1.21 |

|

November,08

|

15.9

|

-0.74

|

|

December,08

|

15.7

|

-1.12

|

|

Average Monthly

change |

|

-1.01

|

Table

1 >> Click

to Enlarge

These trends in Asia are of significance because at

the time when the crisis was just beginning to unfold,

optimists pointed to Asia as the shock absorber that

would buffer the global downturn. A decoupled Asia,

it was argued, would through its own growth and the

demands that it would make on the world's output ensure

that the financial crisis that was largely a phenomenon

restricted to the developed countries would not have

as damaging an effect on global growth as the pessimists,

then in a minority, were predicting.

Chart

4 >> Click

to Enlarge

Implicit in this confidence was the view that Asia

was a region where the turn to market friendly policies

was undertaken in a form and at a pace that had strengthened

these economies and delivered an ''Asian century''.

When sceptics pointed to the East Asian financial

crisis, they were countered with the view that 1997

was an aberration that resulted from ''cronyism''

or some such intangible and not from liberalisation

and global integration.

Table

2: Percentage change in Employment of Exporting

and Non-Exporting units

|

|

Exporting

Units |

Non-

Exporting Units |

Overall

|

|

October,08

|

-1.3 |

-1.05 |

-1.21 |

|

November,08

|

-0.45 |

-1.24 |

-0.74 |

|

December,08 |

-1.66 |

-0.15 |

-1.12 |

|

Average Monthly

Change |

-1.13 |

-0.81 |

-1.01 |

Table 2 >> Click

to Enlarge

It needs noting that the damage wrought by early liberalization

had forced many Latin American countries to search for

alternative strategies. The resulting turn in economic

policy-making in Latin America has had positive consequences.

In the past a crisis in the US and other developed countries

proved damaging for Latin American countries dragging

them down to degrees far greater than the crisis in

the developed countries itself. However, this time around,

growth in the developing countries of the Western Hemisphere,

which was estimated at 5.7 and 4.6 per cent in 2007

and 2008, is expected to fall to a positive 1.1 per

cent in 2009. That is, the continent seems to have escaped

the kind of contraction it was prone to in the past,

when the global economy faced crises of even lesser

intensities.

It was the poor performance of much of Africa and Latin

America since the 1970s that resulted in Asia emerging

as its showcase, with global capital talking up these

economies and attempting to garner the support of domestic

elites for more liberal policies. As success accompanied

each turn in policy, the shift to a regime that opened

these economies to trade, foreign direct investment

and purely financial flows intensified. Asia came to

symbolise the benefits to be derived from liberalisation

and global integration, and epitomise the view that

the world is flat with no walls to climb.

Over the last two decades and more this shift towards

more open strategies has indeed transformed Asia's relationship

with the rest of the world. While the region was earlier

home to a few mercantilist, export-oriented economies

like Japan, South Korea and Taiwan (Province of China),

in time every Asian economy, including the biggest,

was looking for a market abroad with some like China

proving extremely successful in manufacturing and others

like India in services. Moreover, while Asia could be

proud of a high degree of regional integration through

trade and investment flows, this integration reflected

not the decoupling of Asia from the rest of the world

but the creation of an export platform in which multi-country

production networks created products that were targeted

at world markets. Production processes were segmented,

and each segment located at appropriate sites that generated

intermediate products that were combined at the final

location ( such as China) to be shipped abroad. The

other impact of the process of liberalisation and integration

was a sharp increase in foreign investment flows to

the region, including large inflows of portfolio capital.

A concomitant of this inflow was the liberalisation

of rules regarding the presence and operation of foreign

firms, including financial firms like banks, merchant

banks, insurance companies, hedge funds and private

equity firms. Capital inflows in many countries in the

region were far in excess of that needed to finance

their current account deficits. In fact, some countries

with current account surpluses were also recipients

of large capital inflows.

Given such integration, it is not surprising that an

Asia that was experiencing robust growth till recently

has been affected quite adversely by the global financial

and economic crisis. As the financial crisis unfolded,

foreign financial investors in need of capital to cover

losses and meet margin calls at home unwound their positions

in Asia resulting in a collapse in stock markets in

many Asian economies. Countries like China, India and

Vietnam which had seen their stock markets outperforming

their global ''competitors'' were also the ones that

recorded the steepest falls. The outflow of capital

put pressure on many currencies, forcing central banks

to unwind a part of their reserves. A liquidity and

credit contraction ensued. Foreign financial institutions

that were located in these countries and were facing

difficulties in global markets had to downsize or close,

leading to ripple effects in domestic economies. Domestic

financial institutions exposed to sub-prime mortgage

related assets recorded large losses. Finally, the global

economic recession slowed export growth in these increasingly

export-driven economies. All this generated an Asian

version of the global financial and economic crisis,

which is what the collapse in aggregate growth figures

reflects.

|

| |

|

Print

this Page |

|

|

|

|