Democracy yields many dividends. Important among them

is the pressure on governments, however neo-liberal

in inclination, to pay heed to sentiments that can

determine political legitimacy and make a difference

to electoral outcomes. Over the last year, it has

been obvious that the economic decision-makers within

the UPA government have a strong preference for neo-liberal

policies. Yet, they have had to accept, even if with

much reticence and hesitation, that markets are often

prone to fail, necessitating intervention by the state.

Among the few areas where such good sense appears

to now prevail is the direction of credit to priority

sectors.

A draft Technical Paper prepared by an internal working

group of the Reserve Bank of India (RBI) has recommended

correcting the dilution of priority sector credit

provision. The constitution of the working group was

triggered by a December 2004 decision to revitalise

priority sector credit, which was followed by a reference

in the Annual Policy Statement of the Reserve Bank

of India to a view that enlargement of areas eligible

for priority sector lending had resulted in a loss

of focus and that ''credit growth in housing, venture

capital and infrastructure has been strong while it

has been sluggish in agriculture and small industries.''

The working group's mandate therefore was to revisit

the need for priority sector lending and assess the

demand for course correction in the implementation

of the programme.

Since the mid-1960s, credit has been seen as an important

instrument of development policy in India. The agrarian

crisis of 1964-66, the industrial deceleration and

overall economic stagnation that followed and the

political instabilities these generated, brought home

the point that crucial institutional constraints to

growth had not been addressed during the early planning

years. This had not only resulted in a development

impasse, but necessitated attention to the deep inequities

that characterised whatever development that had occurred.

Though this realisation did not trigger any fundamental

institutional reform, such as the redistribution of

land, it ensured the adoption of at least some much-needed

policy initiatives, among which was a programme of

priority sector lending. It was clear by then that

India's then predominantly privately owned banking

system was not geared to or interested in delivering

credit to a range of sectors outside of large industry.

Influenced by the fact that credit was an important

component of the Green Revolution ''package'' aimed

at stimulating agricultural growth, and confronted

by the sectoral and unit-wise concentration of credit

delivery, a decision was taken in 1967-68 to consciously

direct credit to priority sectors such as agriculture,

small-scale industry and exports.

After 1969, when 14 major commercial banks were nationalised,

the government went much further in this direction.

In the event, the priority sector was defined to include

Agriculture, Small Scale Industry, Small Road and

Water Transport Operators, Retail Trade, Small Business,

Professional and Self Employed Persons, State sponsored

schemes for Scheduled Castes/Scheduled Tribes, Education,

Housing and Consumption.

However, among these sectors the emphasis was to be

on agriculture, small industry and small business.

At present, the programme requires that priority sector

advances should constitute 40 per cent of net bank

credit (NBC) of domestic banks. The sub-target for

the agricultural sector stands at 18 per cent of total

advances. Further, 60 per cent of advances to the

small scale sector are expected to be directed to

the tiny sector. And, 10 per cent of net bank credit

has to be directed towards weaker sections. (The requirement

set for foreign banks was lower—at 32 per cent—and

the sectoral composition too was more lenient.)

However, over the last decade, financial liberalisation

has been diluting the directed credit programme, partly

by redefining the priority sector or providing alternatives

such as Rural Infrastructure Development Fund (RIDF)

bonds as a substitute for priority sector lending.

Moreover, special targets for the principal priority

areas have been missed. Thus, during the period 2001-04,

the total outstanding credit to the agricultural sector

extended even by public sector banks was within the

range of 15-16 per cent of NBC as against the target

of 18.0 per. Though in respect of private sector banks,

the ratio of agricultural credit to NBC increased

from 7.1 per cent to 11.8 per cent, it still was below

target.

Further with banks allowed to lend to seed and input

supplying companies or invest in RIDF bonds, the share

of direct finance to agriculture in total agricultural

credit declined from 88.2 per cent in 1995 to 71.3

percent in 2004. The share of credit for distribution

of fertilizers and other inputs which was at 2.2 per

cent in 1995 increased to 4.2 per cent in 2004 and

the share of other types of indirect finance from

4.8 per cent to 21.0 per cent. Further, credit to

the SSI sector as a percentage of NBC declined from

13.8 per cent to 8.2 per cent. Much of this credit

went to larger SSI units, as suggested by the fact

that the number of SSI accounts availing of banking

finance declined from 29.6 lakh to 18.1 lakh.

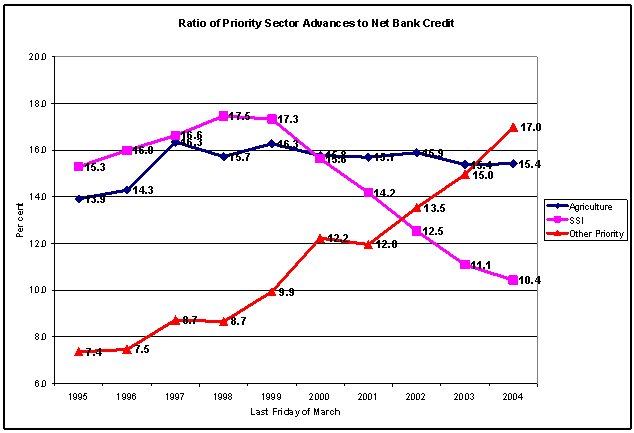

The most disconcerting trend was the sharp rise in

the role of the ''other priority sector'' in total

priority sector lending. This sector includes: loans

up to Rs. 15 lakh in rural/ semi-urban areas, urban

and metropolitan areas for construction of houses

by individuals; investment by banks in mortgage backed

securities, provided they satisfy conditions such

as their being pooled assets in respect of direct

housing loans that are eligible for priority sector

lending or are securitised loans originated by the

housing finance companies/banks; and loans to software

units with credit limit up to Rs. 1 crore. Not surprisingly,

the ratio of ''other priority sector'' lending to

net bank credit rose from 7.4 per cent in 1995 to

17.4 per cent in 2005.

All this occurred even though the priority sector

was by no means principally responsible for non performing

assets (NPAs) in the banking system. NPAs under the

priority sector accounted for 47.5 per cent of total

NPAs in 2004. Even though, this was slightly higher

than the share of the sector in total advances (44

per cent) it was by no means disturbingly disproportionate,

given the presumption that these were ''weaker'' sectors

eligible for cross-subsidisation.

In the circumstances, the RBI's decision to correct

course, especially given signs of agrarian distress

and rising SSI mortality, seems natural. Yet, for

the RBI, the constitution of the working group and

its decision to recommend persisting with and strengthening

the priority sector lending programme is indeed a

major step forward. Financial liberalisation, which

the central bank spearheads in tandem with the Ministry

of Finance, seeks to refashion India's financial structure

in directions that require the dismantling of priority

sector lending. In 1991, the early days of unthinking

''reform'', the Narasimham Committee on the Financial

System had argued that, though directed credit programmes

had extended the reach of the banking system to cover

sectors that had earlier been neglected, the use of

the banking system to support priority sectors and

weaker sections was fundamentally misplaced. That

objective the Committee felt should the remit of the

fiscal rather than the credit system. It, therefore,

recommended that directed credit programmes should

be phased out. At most, 10 per cent of aggregate credit,

as opposed to the prevailing norm of 40 per cent,

could be directed, and targeted at a priority sector

redefined to include only small and marginal farmers,

the tiny sector of industry, small business and transport

operators, village and cottage industries, rural artisans

and other weaker sections.

Given the evidence that some of these were the sectors

which received the lowest share of priority lending

even during the heydays of directed lending, such

targeting was a prescription for dismantling the system.

That was understandable within the Narasimham framework,

which saw directed credit as unjustified. But ground

realities prevented the implementation of the Narasimham

recommendations. And changed economic and political

conditions have now forced the RBI to revisit the

implementation of the programme.

In fact, the working group starts by once again posing

the question as to whether such credit is needed at

all. Thankfully, its answer is yes. But given the

predilections of the central bank, the justification

provided for that answer is weak and even contrary.

There are two levels at which the justification can

rest. The first is on grounds of equity alone. All

sectors must get a fair share of credit, however 'fair'

be defined. It is clearly on this ground that the

working group advances its case for persisting with

directed credit. To quote the working group's draft

report: ''Even after 36 years of priority sector lending

prescriptions, it is observed that certain important

sectors in the economy continue to suffer from inadequate

credit flow…. As such, the need for having priority

sector prescriptions continues to exist.''

While equity is indeed a valid objective in itself,

the second and more important reason why priority

sectors are delineated and supported with directed

credit (sometimes even at lower interest rates) is

that credit concentration is inimical to balanced

development, which in the medium term keeps overall

growth below its potential. It could either result

in inadequate supplies in sectors crucial to development,

that hold back the expansion of the more ''dynamic''

ones; it could limit the expansion of incomes and

the market and therefore of production.

For example, because of differentials in profitability,

the allocation of investment may not be in keeping

with that required to ensure a certain profile of

the pattern of production, needed to raise the rate

of saving and investment as emphasised in India by

the Mahalanobis model. An obvious way in which this

happens is through inadequate investments in the infrastructural

sector characterised most often by lumpy investments,

long gestation lags, higher risk and lower profit.

Given the ''external benefits'' associated with such

industries, inadequate investments in infrastructure

would obviously constrain the rate of growth. Overall,

the private-profit driven allocation of credit for

investment could aggravate the inherent tendency in

markets to direct credit to non-priority and import-intensive

but more profitable sectors, to concentrate investment

funds in the hands of a few large players and direct

savings to already well-developed centres of economic

activity.

Finally, even in developing countries which choose

a mercantilist strategy of growth based on the rapid

acquisition of larger shares of segments of the world

market for manufactures, the government must ensure

an adequate flow of cheap credit to chosen firms.

This needs to be done so that they can make investments

in frontline technologies and internationally competitive

scales of production and would have the wherewithal

to survive during the long period when they build

goodwill in the market.

It is for these reasons that directed credit programmes

were and continue to be adopted by late industrialising

countries. This seems to be recognised by the draft

report, inasmuch as it surveys the experience with

directed credit of a select sample of countries such

as China, Japan and South Korea. However, the emphasis

of the survey is not the importance of directed credit

in the development of these countries, but on the

problems confronted in implementing directed credit

programmes. The ''findings'' of the survey are discouraging:

risks of default on priority lending are high; targeting

results in diversion of funds to non-priority purposes;

differential interest rates increase the cost of credit

for non-preferred borrowers and distort (rather than

correct distorted) incentive structures; and, once

introduced, priority lending is difficult to dispense

with. Given this litany of problems with directed

credit, the working group's case for continuing with

priority sector lending appears to be a contradiction.

At best it appears to be the better of two evils:

iniquitous lending and distorting interventionism

in credit markets.

Fortunately, this has not prevented the working group

from recommending that the priority sector lending

programme should not just continue at the current

level, but be restructured. It calls for focus on

direct and not indirect lending to agriculture, for

rendering mediated lending to the small scale sector

or lending for creation of industrial estates is ineligible

for priority status, and for substantially reducing

the width of ''other'' priority sectors by excluding

areas like housing and consumption loans and loans

to SHGs/NGOs, the food and agro-based processing sector

and the software industry.

The recommendation to remove advances to SHGs/NGOs

and microfinance institutions from the priority category

is particularly significant. The enforced retreat

of the banks from rural credit provision under financial

liberalisation has been accompanied by an emphasis

on microcredit. But experience has shown that high

transaction costs make such credit extremely expensive

and inadequate to finance productive activity. But

now, the pressure to use the credit mechanism as an

instrument of the state is obviously strong enough

for the working group to recognise that microfinance

is no substitute for lending by the formal banking

sector. Hopefully, these conclusions and recommendations,

and not the working groups views on the experience

with directed credit worldwide, would be the basis

for future policy.

Chart

>> Click

to Enlarge