Jobless Growth in Chinese Manufacturing

China is increasingly seen as the manufacturing powerhouse of the developing world, to which manufacturing jobs from the North are increasingly being transferred. However, the actual evidence on Chinese employment shows a somewhat different recent reality.

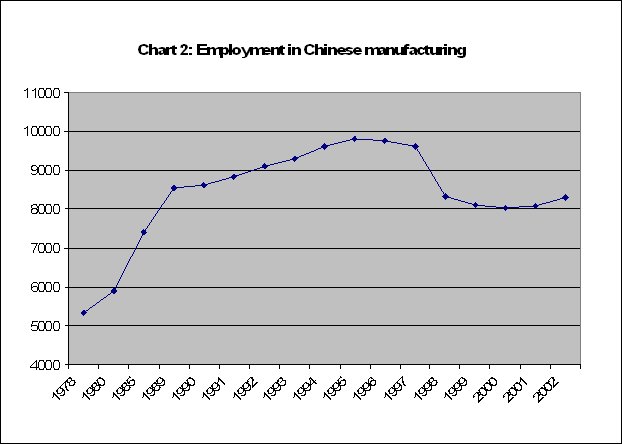

To begin with, in the past two decades, the share of the secondary sector in total employment has changed very little, increasingly only from 20.8 per cent in 1985 to 23 per cent in 1995 and to just 23.8 per cent in 2005. This is despite the fact that though the share of the secondary sector in GDP increased to reach 47.5 per cent in 2005.

Much of this is because the pattern of growth has been – as elsewhere in the world – much less labour-absorbing than in the past. Overall, employment elasticities of output growth have been low, as shown in Table 1. But more to the point, they appear to have fallen sharply in the 1990s compared to the previous decade.

It is predictable that primary sector employment elasticities will be low, and indeed they turned negative in China in the 1990s. However, even industrial employment generation has been very inelastic, and the elasticity has fallen by five times between these decades, to only 12 per cent over the 1990s. This explains the low aggregate employment elasticity to GDP for China as a whole over the decade until 2000.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||

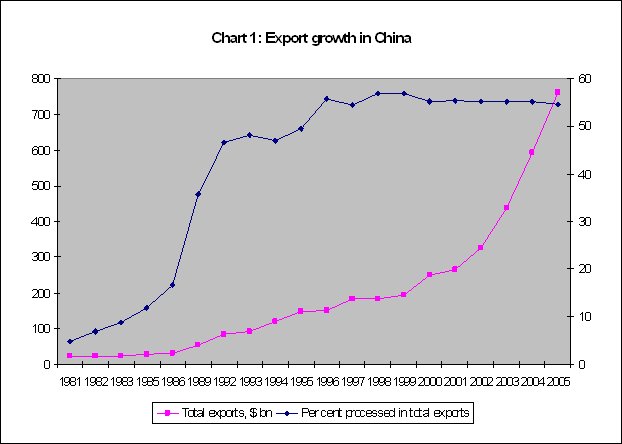

For any other developing country such figures would hardly be surprising, but China has become synonymous internationally with rapid economic growth based on the export of relatively more labour-intensive commodities. This naturally leads to the expectation that manufacturing growth will be such as to generate relatively more employment, and that the employment elasticity of manufacturing output at least would be relatively high.As Chart 1 shows, the exports have grown dramatically in the past ten years in particular, and within that the share of processing exports has increased sharply also in the last decade, going from less than 20 per cent of the total value of exports in the 1980s to more than 55 per cent in the most recent period. Processing exports are seen as generating less value added but more employment, and therefore more likely to involve more employment generation than resource-based or capital-intensive exports. This makes it all the more to be expected that the pattern of Chinese growth would be such as to create more employment in manufacturing.

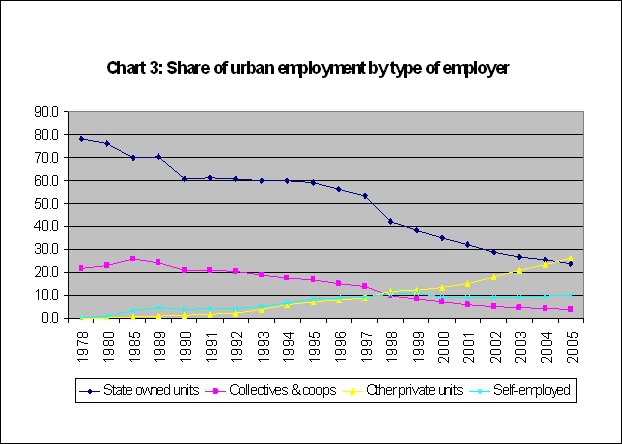

While a high level of employment was sustained in the past by the state’s policy of keeping surplus workers in both SOEs and agricultural collectives, this policy was abandoned in the mid-1990s in the move towards a market economy. In a more competitive atmosphere, the SOEs and collectives have also had to restructure their operations and adopt more capital-intensive technologies. When the number of laid off workers, most of whom are from these units, is included in the official unemployment figures, the actual rate is much higher at around 12.5 per cent of the working population in 2000. This in any case does not include most of the migrants from the rural sectors, many of whom are underemployed.

However, the growth in China has been accompanied by rising real wages. Table 2 indicates relatively buoyant increases in real wages across various types of employment units, in most of the years since 1978. These wages have been particularly marked in the current decade.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

However, it should be noted that these real wage data refer to organised sector workers, and leave out the increasing proportion of unorganised workers, most particularly the rural migrants who operate in the most oppressive labour market conditions in urban China. A large survey organised by the Chinese Academy of Social Sciences revealed that in 2005 a majority of migrant workers typically faced long hours of work for all days of the week, for less than minimum wages and with poor residential conditions. Therefore it is unlikely that the real wage increases evident for organised sector workers would have been matched by similar increases for unorganised workers, especially migrants.

The basic accumulative thrust therefore appears to be relying on investment driven by rising profit shares (similar to some “exhilarationist” models of economic growth) and generating less employment per unit of investment or output. The apparent disjunction between economic growth and employment generation in China is something that has been experienced by a number of other export-oriented developing countries already. Indeed, China was earlier something of an outlier in that, it showed continuously expanding manufacturing employment despite greater trade openness. Under an open economic regime, the responsiveness of employment growth to the growth in output typically declines.

There are several reasons for this. The most obvious is the impact of trade liberalisation on the pattern of demand for goods and services within the country. As tastes and preferences of the elites in developing countries are influenced by the “demonstration effect” of lifestyles in the developed countries, new products and processes introduced in the latter very quickly find their way to the developing countries when their economies are open.

Further, technological progress in the form of new products and processes in the developed countries is inevitably associated with an increase in labour productivity. Producers in developing countries find that the pressure of external competition (in both exporting and import-competing sectors) requires them to adopt such technologies. Hence, after external trade has been liberalised, labour productivity growth in developing countries is more or less exogenously given and tends to be higher than prior to trade liberalisation.

So in China as in other developing countries like India, the point is to ensure that jobs are continuously created in the economy in other activities. A critical requirement for this is public expenditure, especially (but obviously not exclusively) in the social sectors. This is typically much more employment-generating than several other economic activities, and therefore also has substantial multiplier effects. There is therefore a strong case for evolving a growth strategy that allows and encourages labour productivity increases overall while significantly expanding expenditure – and therefore income and employment opportunities – in social sectors that positively affect the conditions of life of most citizens.