Themes > Features

11.05.2007

Who is Doing the Saving and Investing?

Since

the turn of the century, the Indian economy is widely perceived to be

on a rapid growth trajectory that is significantly faster than that of

the previous decade. Certainly, the National Accounts Statistics of the

CSO show that in the period 1999-2000 to 2006-07, GDP in constant prices

increased at an average annual rate of nearly 7 per cent.

This growth is also clearly driven by higher investment, since investment rates in the economy also appeared to have gone up in this period. But what exactly has caused this shift to what appears to be a higher growth trajectory? In particular, why have investment rates increased? Is this the cause or the result of the higher growth? And what implications does the answer have for the nature of the economic growth process itself?

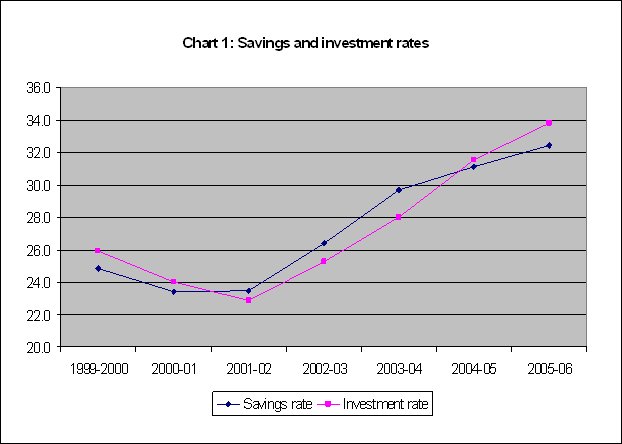

To consider these issues, it is necessary to examine first of all the recent trends in investment and savings rates. Chart 1 shows domestic savings and investment as percentages of GDP at current market prices. Two features emerge clearly. First, until 2002, both savings and investment rates were not on a clear upward trend – indeed, they fluctuated around levels broadly similar to those of most of the 1990s. It is only from 2002 onwards that there is a clear tendency for rapidly rising savings and investment rates. But it is true that the increase over the past four years has been remarkable, with investment rates apparently reaching the levels in several of the fast growing East Asian economies during their period of economic boom.

Secondly, even in this phase of higher growth, for several years domestic savings rates were higher than domestic investment rates, indicating excess savings that were not finding adequate outlet in investment within the economy. So the bullish animal spirits of entrepreneurs were clearly not so strong as to lead to even higher investment rates that were easily feasible given the rising domestic savings. It is only in the very recent past that domestic investment has been higher than domestic savings.

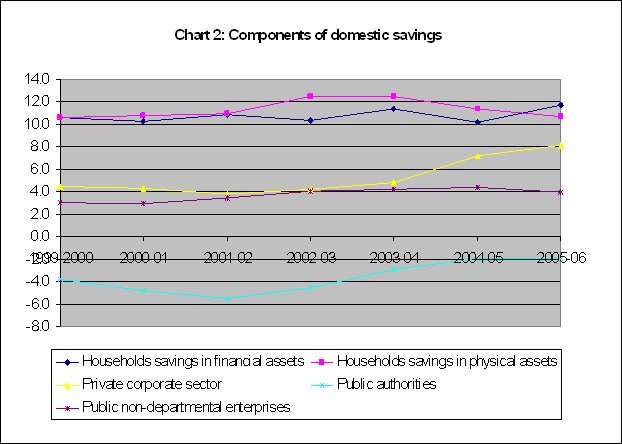

This means that it may be necessary to explain the increase in domestic savings as a first step. Chart 2 decomposes domestic savings into the main constituent parts, as share of GDP. This shows a pattern that is rather different from the 1990s. In the 1990s, the moderate rise in savings rates was led by household savings in physical assets. Since the turn of the decade, the increase in savings rates has been driven by a reduction in the net dissaving of the government (even excluding Public Sector Enterprises) and significant increases in private corporate savings as percentage of GDP.

This very large increase in private corporate savings - a doubling of the rate in around five years - reflects the dramatic increase in profitability over this same period, as shown by the data from the Annual Survey of Industries. It reiterates the conclusion, evident from the ASI, that the private corporate sector has been the chief beneficiary of the economic boom.

Household savings in physical assets covers not only house construction and other building up of physical assets by households, but also real investment in agriculture as well as by the non-agricultural small scale sector, which is not part of the private corporate sector. This measure of savings can therefore be a useful indicator of investment by the numerical bulk of enterprises (which also happen to employ the bulk of the work force in the country). It is therefore notable that this has actually been declining as a share of GDP in the recent past. Since a real estate and construction boom has occurred over this same period, the decline is unlikely to have been in this area. Rather, this suggests that real investment by agriculturalists and small enterprises has come down as a share of GDP, despite the apparent macroeconomic boom.

It is also worth noting that savings by public enterprises have also increased over this period, and the negative savings of the public authorities (which includes government per se and departmental enterprises) has reduced.

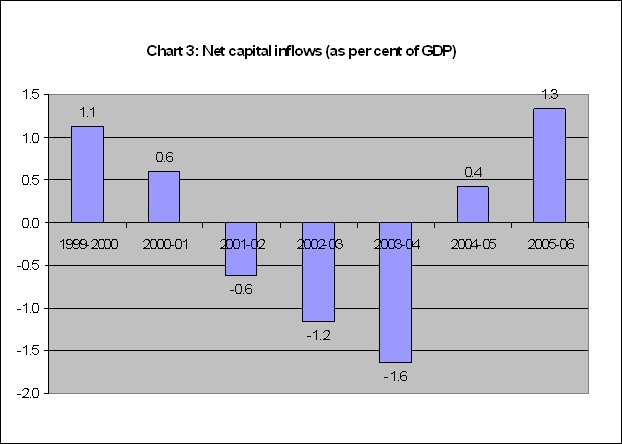

It is often argued – even by important policy makers and government leaders – that external capital is essential to allow the Indian economy to grow, and that therefore it is critical to undertake various measures to encourage more FDI and more portfolio investment into the economy. Yet, as Chart 3 indicates, net capital flows have been negative for a significant part of the recent period of high aggregate growth. Indeed, they were negative and falling when domestic investment rates were increasing quite sharply.

Even when net capital inflows have turned positive, as in the very recent past, they still form a negligible proportion of the investment and certainly a minuscule proportion of GDP. They cannot be said to have added significantly to domestic savings such as to ensure higher investment rates, since their contribution has been either negative or marginal.

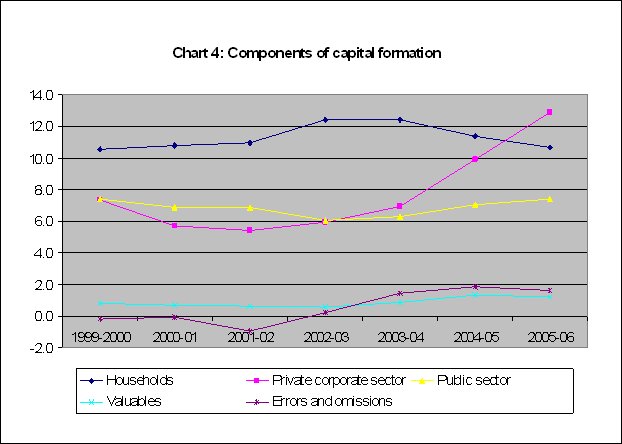

The conclusions that emerge from the decomposition of savings are reinforced by an examination of the components of investment. This is shown in Chart 4. Investment by households (which includes, as mentioned above, all non-corporate investment in agriculture as well as investment by non-corporate small units in industry and services) has been the major component of gross domestic savings for a long time. It increased in proportion of GDP between 1999 and 2002, but subsequently has been declining. In fact, in 2005-06 it was actually overtaken in importance by investment of the private corporate sector, which has increased very sharply from the same period. Public sector investment has remained broadly stable as a proportion of GDP. The relatively new term "valuables" is an attempt to capture the holding of gold and other precious stones and metals. It is a moot point whether this should be included in investment, since it is not real productive investment as much as a form of hoarding. Of course, its share of total domestic investment remained small even in 2005-06, at less than 4 per cent. But its share has been increasing from less than 1 per cent two years earlier, and would therefore have contributed to the overall increase in aggregate investment rates, even if its actual role is notional.

Errors and omissions also appear to have been growing and are now quite significant, amounting to nearly 5 per cent of gross domestic investment. But it is difficult to know what to make of this increase and how to interpret it.

What all this suggests is that the recent boom has been driven by the private corporate sector’s increasing role in both domestic savings and investment. And this in turn has been driven by the increase in corporate profitability which has been especially marked since 2002. The sharp increase in corporate profits (based on ASI data) was discussed in an earlier paper.

The increase in corporate profitability in turn is not a sui generis phenomenon, arising simply out of the growth process itself. Rather, it is the outcome of government policies. It can be explained by the combination of the low interest rates and numerous tax concessions and implicit subsidies that have significantly increased retained profits over this period.

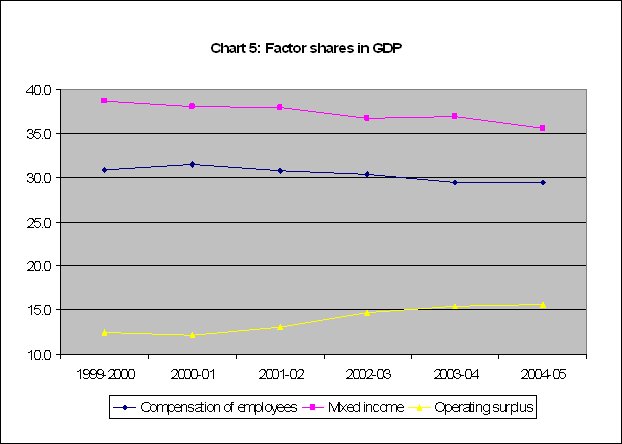

The increasing share of profits is confirmed by CSO data on factor shares in national incomes, as described in

Chart 5.

From Chart 5 it is evident that the share of operating surplus of companies (which incidentally includes both private and public enterprises) has increased from around 12 per cent at the start of the decade to nearly 16 per cent in 2004-05, which is a remarkable increase of around 30 per cent in a very short time. At the same time, the share of employees compensation has come down marginally. This includes both workers wages, which have come down quite sharply, and remuneration of salaried employees, which has gone up.

Meanwhile, the category "mixed income" shows a declining trend in income share, and over the period in question the share fell by around 8 per cent. This is significant because this includes all the self-employed, who have been growing as a proportion of the employed and who now account for half the work force in India according to the latest NSS large survey. So, even while the share of population dependent upon "mixed income" has increased, the share of income received by this group has fallen.

So this is a profit-led boom, driven by increasing inequality not only between workers and capitalists, but also between different categories of producers. The private corporate sector is the greatest beneficiary and now also the greatest contributor to the boom. But the non-corporate producers and small and tiny establishments, as well as petty self-employed producers of goods and services, are clearly not gaining in relative terms, and in some cases may be worse off absolutely.

This allows us to relate the macroeconomic and national accounts data to the evidence from the employment surveys, of falling shares and worsening conditions of wage employment over this period. It also allows us to understand why the theme of "two Indias" is unfortunately so persistent and so plausible, at least in economic terms.

This growth is also clearly driven by higher investment, since investment rates in the economy also appeared to have gone up in this period. But what exactly has caused this shift to what appears to be a higher growth trajectory? In particular, why have investment rates increased? Is this the cause or the result of the higher growth? And what implications does the answer have for the nature of the economic growth process itself?

To consider these issues, it is necessary to examine first of all the recent trends in investment and savings rates. Chart 1 shows domestic savings and investment as percentages of GDP at current market prices. Two features emerge clearly. First, until 2002, both savings and investment rates were not on a clear upward trend – indeed, they fluctuated around levels broadly similar to those of most of the 1990s. It is only from 2002 onwards that there is a clear tendency for rapidly rising savings and investment rates. But it is true that the increase over the past four years has been remarkable, with investment rates apparently reaching the levels in several of the fast growing East Asian economies during their period of economic boom.

Secondly, even in this phase of higher growth, for several years domestic savings rates were higher than domestic investment rates, indicating excess savings that were not finding adequate outlet in investment within the economy. So the bullish animal spirits of entrepreneurs were clearly not so strong as to lead to even higher investment rates that were easily feasible given the rising domestic savings. It is only in the very recent past that domestic investment has been higher than domestic savings.

This means that it may be necessary to explain the increase in domestic savings as a first step. Chart 2 decomposes domestic savings into the main constituent parts, as share of GDP. This shows a pattern that is rather different from the 1990s. In the 1990s, the moderate rise in savings rates was led by household savings in physical assets. Since the turn of the decade, the increase in savings rates has been driven by a reduction in the net dissaving of the government (even excluding Public Sector Enterprises) and significant increases in private corporate savings as percentage of GDP.

This very large increase in private corporate savings - a doubling of the rate in around five years - reflects the dramatic increase in profitability over this same period, as shown by the data from the Annual Survey of Industries. It reiterates the conclusion, evident from the ASI, that the private corporate sector has been the chief beneficiary of the economic boom.

Household savings in physical assets covers not only house construction and other building up of physical assets by households, but also real investment in agriculture as well as by the non-agricultural small scale sector, which is not part of the private corporate sector. This measure of savings can therefore be a useful indicator of investment by the numerical bulk of enterprises (which also happen to employ the bulk of the work force in the country). It is therefore notable that this has actually been declining as a share of GDP in the recent past. Since a real estate and construction boom has occurred over this same period, the decline is unlikely to have been in this area. Rather, this suggests that real investment by agriculturalists and small enterprises has come down as a share of GDP, despite the apparent macroeconomic boom.

It is also worth noting that savings by public enterprises have also increased over this period, and the negative savings of the public authorities (which includes government per se and departmental enterprises) has reduced.

It is often argued – even by important policy makers and government leaders – that external capital is essential to allow the Indian economy to grow, and that therefore it is critical to undertake various measures to encourage more FDI and more portfolio investment into the economy. Yet, as Chart 3 indicates, net capital flows have been negative for a significant part of the recent period of high aggregate growth. Indeed, they were negative and falling when domestic investment rates were increasing quite sharply.

Even when net capital inflows have turned positive, as in the very recent past, they still form a negligible proportion of the investment and certainly a minuscule proportion of GDP. They cannot be said to have added significantly to domestic savings such as to ensure higher investment rates, since their contribution has been either negative or marginal.

The conclusions that emerge from the decomposition of savings are reinforced by an examination of the components of investment. This is shown in Chart 4. Investment by households (which includes, as mentioned above, all non-corporate investment in agriculture as well as investment by non-corporate small units in industry and services) has been the major component of gross domestic savings for a long time. It increased in proportion of GDP between 1999 and 2002, but subsequently has been declining. In fact, in 2005-06 it was actually overtaken in importance by investment of the private corporate sector, which has increased very sharply from the same period. Public sector investment has remained broadly stable as a proportion of GDP. The relatively new term "valuables" is an attempt to capture the holding of gold and other precious stones and metals. It is a moot point whether this should be included in investment, since it is not real productive investment as much as a form of hoarding. Of course, its share of total domestic investment remained small even in 2005-06, at less than 4 per cent. But its share has been increasing from less than 1 per cent two years earlier, and would therefore have contributed to the overall increase in aggregate investment rates, even if its actual role is notional.

Errors and omissions also appear to have been growing and are now quite significant, amounting to nearly 5 per cent of gross domestic investment. But it is difficult to know what to make of this increase and how to interpret it.

What all this suggests is that the recent boom has been driven by the private corporate sector’s increasing role in both domestic savings and investment. And this in turn has been driven by the increase in corporate profitability which has been especially marked since 2002. The sharp increase in corporate profits (based on ASI data) was discussed in an earlier paper.

The increase in corporate profitability in turn is not a sui generis phenomenon, arising simply out of the growth process itself. Rather, it is the outcome of government policies. It can be explained by the combination of the low interest rates and numerous tax concessions and implicit subsidies that have significantly increased retained profits over this period.

The increasing share of profits is confirmed by CSO data on factor shares in national incomes, as described in

Chart 5.

From Chart 5 it is evident that the share of operating surplus of companies (which incidentally includes both private and public enterprises) has increased from around 12 per cent at the start of the decade to nearly 16 per cent in 2004-05, which is a remarkable increase of around 30 per cent in a very short time. At the same time, the share of employees compensation has come down marginally. This includes both workers wages, which have come down quite sharply, and remuneration of salaried employees, which has gone up.

Meanwhile, the category "mixed income" shows a declining trend in income share, and over the period in question the share fell by around 8 per cent. This is significant because this includes all the self-employed, who have been growing as a proportion of the employed and who now account for half the work force in India according to the latest NSS large survey. So, even while the share of population dependent upon "mixed income" has increased, the share of income received by this group has fallen.

So this is a profit-led boom, driven by increasing inequality not only between workers and capitalists, but also between different categories of producers. The private corporate sector is the greatest beneficiary and now also the greatest contributor to the boom. But the non-corporate producers and small and tiny establishments, as well as petty self-employed producers of goods and services, are clearly not gaining in relative terms, and in some cases may be worse off absolutely.

This allows us to relate the macroeconomic and national accounts data to the evidence from the employment surveys, of falling shares and worsening conditions of wage employment over this period. It also allows us to understand why the theme of "two Indias" is unfortunately so persistent and so plausible, at least in economic terms.

©

MACROSCAN 2007